South Africa is currently going through immense challenges regarding the importation of ocean consignments, primarily stemming from aggravated freight rates stagnating trade growth. Freight rates for the Shanghai – Durban shipping route have increased almost to three times the levels that they were pre-pandemic. These high freight rates have been heaviest on the shoulders of developing countries, who can least afford it.

Carriers have prioritized vessel capacity for the Far East – American route due to the attractiveness of freight rates prevailing there, translating to greater profitability for these carriers. This in turn has led to the current event that smaller vessels with lower capacity will be servicing the Far East – Southern African shipping lane.

Smaller vessels, denoting less container capacity, have caused an indirect demand shock, and in turn increasing prices along with a decreased supply. A detailed outline of the events that have incurred these shocks is outlined in the following sub-sections.

Savino Del Bene South Africa, along with its Far East counterparts have been working harder than ever to dampen these industry inefficiencies and the effects thereof on our most valued client base. We are dedicated to ensuring that we deliver the superior service our clients deserve.

Kindly note that, should one be willing to accept the prevailing diamond tier rates, vessel space is guaranteed.

Please be aware that these rates will not only be affecting Shanghai, but instead are a reflection to the entire far east ocean trade rates with Southern Africa, likely enough there will be further rate increases for Far East – Southern African ocean trade routes following on from these inefficiencies.

Schedule integrity:

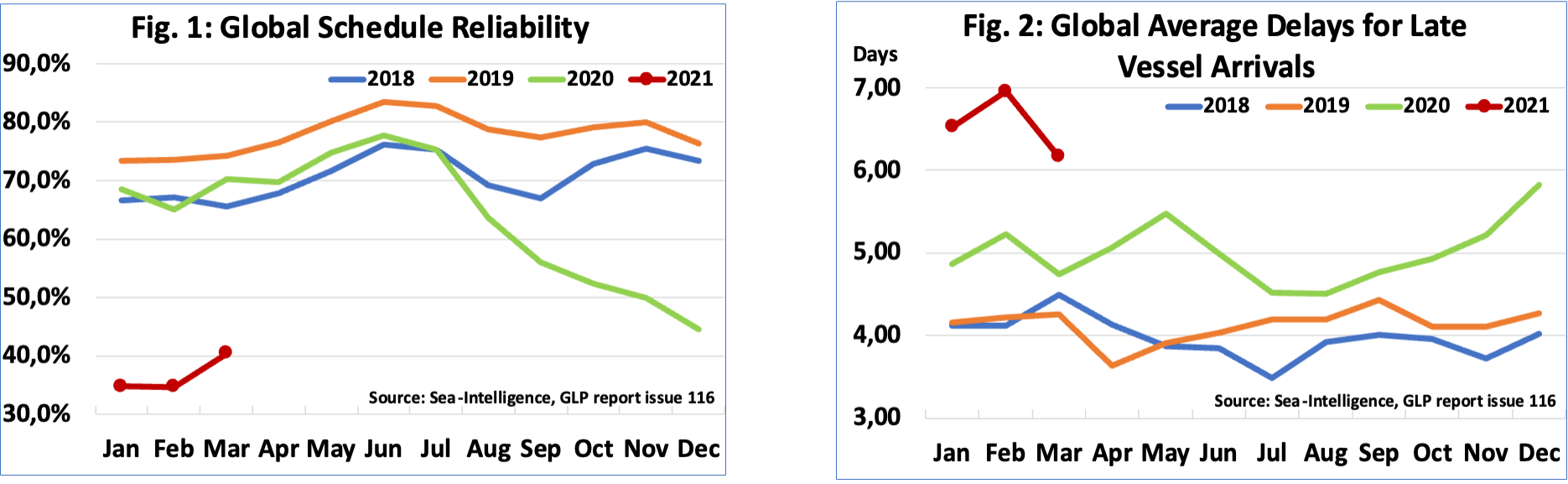

The global vessel schedule reliability has deteriorated drastically over the past year stemming predominantly from the COVID-19 pandemic, only to be magnified by black swan events such as the Suez Canal blockage and unprecedented levels of equipment and space shortages.

According to a leading provider of Research & Analysis, Sea-Intelligence, Global Schedule reliability is down from 70% in March 2020 to a dismal low of 40,4% in March 2021. The Sea-Intelligence press release dated Mar 27th, 2021 outlines that the average delay for late vessel arrivals is 6,16 days for March 2021, whereas in March 2020 this figure was somewhat lower at 4,74 days, translating to 1,42 days higher Y-Y. Effectively being the highest March average recorder in the past 4 years. See Figures 1 & 2 below.

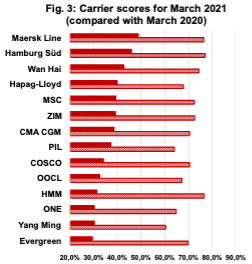

Maersk Line was on a global average the most unwavering in the month of march with a schedule reliability 48,7% with Hamburg Sud coming in second at 45.9%. See Fig. 3 below which is an attestation hereof.

Vessel prioritization:

The second facet explored in breaking down the current pandemonium in the global logistics industry is that of vessel-route prioritisation.

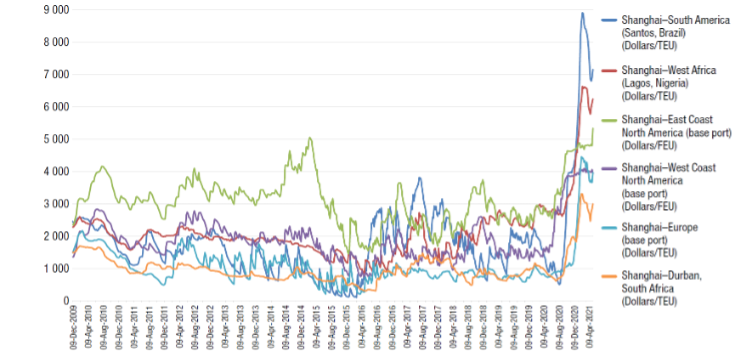

According to the Shanghai containerized freight index, rates prevailing for the Shanghai – South American route are second to none, in contrast, being almost three times more than the rates prevailing for the Shanghai – Durban route. In conjunction, general rates for the Shanghai – East coast route are almost 70% higher than those for the Shanghai-Durban route.

Due to the Shanghai – Durban freight rates being the lowest of them all under question, carriers have decreased capacity on the respective route and reallocated majority of their vessels, including the largest of their fleets, onto the most profitable routes, of which the Shanghai – Durban route is not included.

Figure 4, below, visualises the stark differentials in rates on the various shipping routes as well as the formidable bullish spot rates trend that has come into effect, starting its run in August, 2020.

Figure 4: Shanghai containerized freight index, weekly spot rates, 18 December 2009-9 April 2021.

Source:

UNCTAD calculations, based on data from Clarksons Research, Shipping Intelligence Network Time Series.

Adding to the woes of the above-mentioned vessel prioritization, the number of blank sailings that have prevailed in the past 5 months have only increased the strain on Southern African trade. More blank sailings have been observed in the first half of this year (2021), than those that occurred in the whole of last year (2020).

Demand outweighing supply:

The resulting schedule integrity and vessel prioritization, as in the afore mentioned, are resulting in a major imbalance in demand and supply of containerized consignments.

The schedule integrity is ultimately leading to an increase in lead times for transshipments and direct shipments from the far east to Southern Africa and coupled with an already exasperated logistics industry in Southern Africa the effects hereof are only intensified.

The decreased supply capacity due to smaller vessels servicing the Southern-Africa route, subsequent of lowered profitability for liners, are spurring on a contrasted increase on demand for vessel space.

Increased freight rates:

As a result of the outweighed demand on supply, caused by the above external shocks, economical models dictate that rates will inevitably increase, which has indeed been observed. These increased rates have been most damaging to developing regions especially, such as South Africa, as they are the ones whom can least afford it.